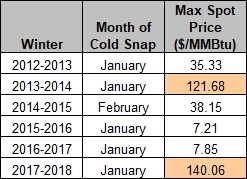

In Part I, we looked at some data from the most recent 2018 cold snap in the North American East to find out that during the event, the natural gas production glitches were major contributors to the supply shortage. On some hubs, prices jumped above $100/MMBtu.

In our quest for an explanation of the natural gas industry failure to properly respond to the cold snap and possibly develop forecasts assisting in dealing with and preventing such expensive outcomes, we decided to examine how unique the situation in winter 2018 was. So, we looked at the historical data in New York between winters 2013 and 2018.

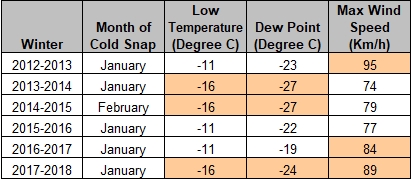

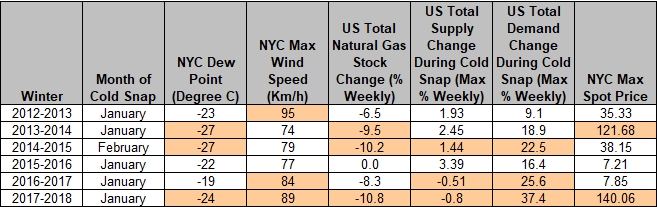

The first question we needed an answer for was whether inconsistent temperature patterns could be responsible for the recurring winter dramas. The short answer was “Not really”. Winter storms are consistent and can be predicted easily. Every winter, between years 2013 and 2018, New York experienced cold snaps with temperature declining to -11C… -16C (-27C with Dew Point) and wind strengthening into the 90s km/h, as shown in Figure 1: Temperature and Wind Speed in New York During Cold Snaps. Winters of 2014, 2015 and 2018 were the coldest on the record with the strongest winds blowing in 2013, 2017 and 2018.